Overview of Both Income Tax Systems

The United Kingdom and the United States have fundamentally different approaches to taxation, though both are progressive systems. A progressive system naturally means that higher earners pay increasingly higher percentage rates. Understanding these distinct differences is crucial for expatriates, international workers, and global businesses. If you plan to move across the Atlantic, your entire financial strategy must drastically adapt to the new rules.

Both nations fund public services through these ongoing income levies. The US uses taxes to fund federal programs, defense, and infrastructure. The UK similarly funds infrastructure, but crucially uses a massive portion to universally fund the National Health Service. Let us break down exactly how each system handles your hard-earned money.

We will explore the specific brackets, the complex structures, and how your final take-home pay is ultimately calculated. Comparing the two correctly helps you evaluate true earning potential when considering international job offers. It is rarely as simple as comparing the gross salary numbers directly.

The Core Structural Difference

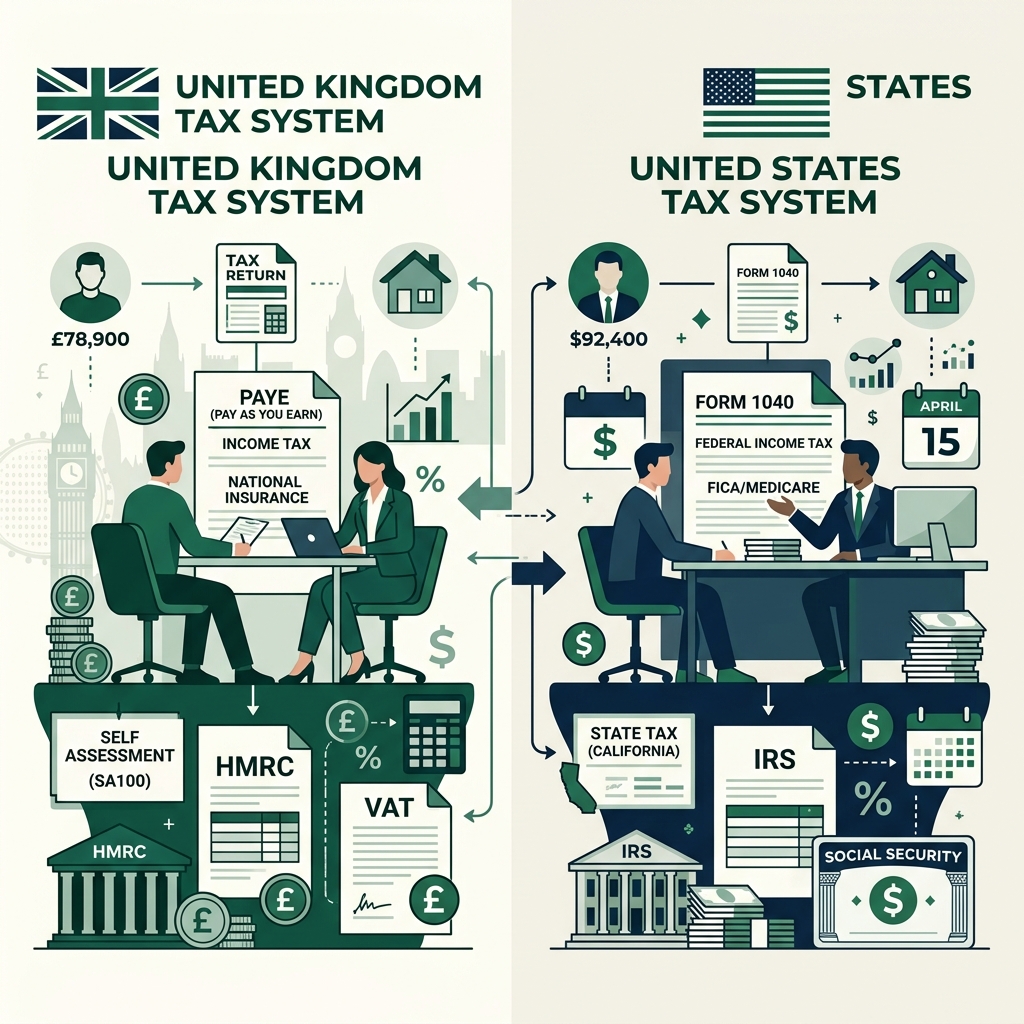

The UK operates on an streamlined PAYE (Pay As You Earn) network. Your employer automatically deducts your precise income tax and National Insurance before you even get paid. For the vast majority of UK residents, absolutely everything is handled accurately and silently. Most ordinary citizens never have to file a formal tax return in their entire lives. Filing a self-assessment in the UK is only strictly required if you have complicated untaxed income, are self-employed, or consistently earn over £100,000 annually.

Conversely, the US exclusively uses a heavily involved withholding system. Your employer estimates your tax liability and systematically withholds that money from your regular paycheck. However, this is barely the beginning. You MUST file an intricate annual return (Form 1040) regardless of how accurate that initial withholding was. This required annual reconciliation is the single most important practical difference for everyday working professionals.

In America, filing taxes is a massive annual event requiring meticulous record-keeping. Many individuals hire dedicated professional accountants just to complete basic yearly compliance. In Britain, the government essentially does all the basic math for standard employees automatically.

Income Tax Rates Side by Side

Both countries utilize distinct tax bands to categorize earnings. Let us look closely at the exact numbers.

UK Income Tax (2025/26)

The UK provides a generous tax-free personal allowance.

- Personal Allowance: £12,570 (0% tax applied)

- Basic Rate: £12,571 – £50,270 (20% tax applied)

- Higher Rate: £50,271 – £125,140 (40% tax applied)

- Additional Rate: Over £125,140 (45% tax applied)

US Federal Income Tax (2026)

The US federal system features many more granular brackets.

- 10%: Up to $11,600

- 12%: $11,601 – $47,150

- 22%: $47,151 – $100,525

- 24%: $100,526 – $191,950

- 32%: $191,951 – $243,725

- 35%: $243,726 – $609,350

- 37%: Over $609,350

Effective Tax Rate vs Marginal Rate

Understanding the difference between effective and marginal rates will fundamentally change how you view your paycheck. Your marginal rate represents the highest mathematical tier your income happens to fall into. For example, consider a completely standard UK worker earning exactly £50,000 annually.

Their total tax on the first £12,570 is exactly £0. The tax applied on the remaining £37,430 (£12,571 to £50,000) is £7,486 at a 20% rate. Their absolute total income tax paid is £7,486. While their stated marginal rate is undeniably 20%, their actual effective taxpayer rate is merely 14.97% (£7,486 divided by £50,000). Your effective rate is always significantly lower than your top marginal rate.

US State Income Tax — the Hidden Layer

Unlike the UK, the US allows individual states to aggressively levy their own income taxes completely separately from the federal government. Interestingly, 9 specific states have absolutely no income tax whatsoever. These states include FL, TX, WA, NV, SD, WY, AK, NH, and TN. Living in Texas saves you thousands compared to high-tax states.

Conversely, California tops out intensely at a 13.3% state rate. Moreover, New York City residents shockingly pay a dedicated city tax heavily stacked on top of their mandatory state tax. A $80,000 earner living in NYC pays federal tax, NY state tax, AND NYC tax. The UK equivalent is simply Council Tax, which is a property-based flat fee, rarely ever linked to income levels directly.

Social Contributions — NI vs FICA

Beyond pure income tax, both nations continuously collect mandatory social contributions to fund specific government services.

| Contribution | UK Rate | US Rate | Maximum Cap Limit |

|---|---|---|---|

| Employee NI (Class 1) | 8% (£12,570-£50,270), 2% above | — | None |

| Social Security (OASDI) | — | 6.2% | $168,600 (2024 Base) |

| Medicare Deduction | — | 1.45% (+0.9% over $200k) | None |

These contributions quickly add up, significantly denting your final monthly take-home pay check.

Filing Obligations — Where It Gets Complicated

The international nightmare truly consistently begins when managing cross-border filing obligations.

US citizens permanently living abroad must file US federal taxes annually, even if they owe absolutely nothing. The US heavily taxes based on citizenship, not mere residency. Provisions like the Foreign Earned Income Exclusion (covering up to $126,500 in 2024) frequently reduce the actual owed liability down to zero. However, failing to file appropriately still triggers immense federal penalties.

Historically, UK non-domiciled residents typically paid tax exclusively on their localized UK income. These legacy rules profoundly changed recently in April 2025. Dual citizens currently face the absolute highest levels of compliance complexity imaginable. They inevitably require expensive specialized accountants to simultaneously navigate both aggressive tax regimes concurrently.

Practical Comparison — Same Salary, Different Take-Home

Let us thoroughly examine a highly concrete example. Say you earn a solid £50,000 entirely in the UK. Next, imagine a rough PPP equivalent salary of exactly $63,000 right in the US. Let us distinctly show the approximate final take-home amounts securely in both situations.

The UK worker routinely takes home roughly £39,000 safely after total income tax and required NI deductions. Everything is systematically managed perfectly by the helpful employer.

The US worker actively living in Texas, intentionally filing as a single adult, proudly takes home roughly $51,000 exclusively after strict federal and FICA taxes. Note well that this is highly approximate, as actual exact final numbers depend intimately on multiple shifting personal factors.

Read more about how bonuses are taxed.

Frequently Asked Questions

Do I have to file taxes every year in the UK?

Most employed individuals in the UK do not file a yearly return. Their taxes are handled entirely automatically through the PAYE system by their employer.

Do US citizens living in the UK have to pay tax to both governments?

Due to the US-UK tax treaty, you generally will not pay double tax. You must file returns in both countries, but foreign tax credits typically offset the US liability.

Which country has higher payroll taxes?

The UK slightly edges out the US on payroll deductions for a middle-income earner, mostly due to higher National Insurance rates compared to FICA limits.

Are health insurance premiums tax-deductible in the US?

Yes, many US employees have health premiums deducted directly from their paycheck pre-tax, which actively lowers their total taxable federal income.

Final Thoughts

Make sure you fully grasp your financial choices by utilizing our free Salary Calculator.

Sources & Citations: Content verified against official guidelines from the IRS (US), HMRC (UK), and ATO (AU). Information is reviewed for accuracy prior to publication.

Try the Salary Calculator

Calculate your exact net salary after tax, NI, and deductions.

Open Calculator →

Comments are coming soon. Have feedback? Contact us.