Every Canadian employee notices it: somewhere around October or November, the paycheque is suddenly larger. No raise, no bonus: just fewer deductions. That's the CPP and EI maximums kicking in. Once your cumulative earnings for the year cross certain thresholds, contributions to the Canada Pension Plan and Employment Insurance stop for the rest of the year. Here's exactly what those thresholds are for 2026, how much you'll save when you hit them, and what the new CPP2 enhancement means for higher earners.

2026 CPP and EI Payroll Caps

CPP1 stops at $73,200 | CPP2 stops at $81,900 | EI stops at $63,200

Once these thresholds are reached, those deductions stop for the rest of the calendar year: your employer is also notified by your payroll software to cease withholding.

2026 CPP and EI: The Complete Numbers

| Deduction | Employee Rate | Earnings Threshold | Max Employee Contribution | Employer Match |

|---|---|---|---|---|

| CPP1 (Base) | 5.95% | $3,500 (exemption) to $73,200 | $3,867.50 | $3,867.50 (matches exactly) |

| CPP2 (Enhanced) | 4.00% | $73,200 to $81,900 | $347.00 | $347.00 (matches exactly) |

| EI | 1.66% | $0 to $63,200 | $1,049.12 | $1,468.77 (2.4× employee rate) |

⚠️ 2026 payroll deduction rates. Source: CRA — CPP Contribution Rates 2026. Employer EI premium rate is 1.4× the employee rate for most employers.

When Do CPP and EI Stop? By Salary Level

The timing depends on your salary and pay frequency. Higher earners hit the caps earlier in the year. Here's approximately when different earners stop paying CPP1: the most common stopping point:

| Annual Salary | CPP1 Stops Approx. | EI Stops Approx. | Monthly Pay Boost After Caps |

|---|---|---|---|

| $50,000 | Never (under cap) | Never (under cap) | N/A — deductions continue all year |

| $73,200 (CPP1 cap) | End of December | October (approx.) | ~$88/month when EI stops |

| $90,000 | Late October | Early September | ~$450/month when both stop |

| $120,000 | Early August | Early July | ~$600/month when both stop |

| $150,000 | Mid-June | Early May | ~$770/month when both stop |

⚠️ Approximate stop months for bi-weekly pay. Exact dates depend on pay schedule and year-to-date tracking. CPP2 continues to $81,900 for those above the CPP1 cap.

Understanding CPP2: The Enhancement Layer

Starting in 2024, the CPP enhancement introduced a second earnings ceiling (Year's Additional Maximum Pensionable Earnings, or YAMPE). Employees earning between $73,200 and $81,900 pay an additional 4% CPP2 contribution on that earnings band. For 2026, this means a maximum CPP2 contribution of $347 for those earning above $73,200.

The CPP2 enhancement means a higher CPP retirement benefit. The CRA projects that when fully phased in, CPP will replace up to 33.33% of your average career earnings: up from the original 25% target. For someone averaging $60,000 in career income, this could mean $20,000/year in CPP benefits at retirement versus the old system's $15,000.

| Earnings Range | Contribution | Rate | Max 2026 | Future Benefit Impact |

|---|---|---|---|---|

| $3,500 – $73,200 | CPP1 (base) | 5.95% | $3,867.50 | Up to 25% income replacement |

| $73,200 – $81,900 | CPP2 (enhanced) | 4.00% | $347.00 | Additional income replacement on top earnings |

| Total max (CPP1 + CPP2) | — | — | $4,214.50 | Combined enhanced CPP benefit |

EI: What You're Actually Buying

EI premiums feel like another tax, but they're actually insurance premiums. Employment Insurance pays benefits if you lose your job, get sick, take parental leave, or need to care for a seriously ill family member. In 2026, regular EI benefits pay 55% of your average insurable earnings, up to a maximum of $695/week (55% of the $63,200 maximum insurable earnings ÷ 52 weeks × 55%).

The number of weeks of benefits you can receive depends on your region's unemployment rate and how many insurable hours you've worked. In areas with higher unemployment, you need fewer hours to qualify. Most employees need between 420 and 700 insurable hours to qualify for regular benefits.

📊 Chart Suggestion: "Timeline chart showing at what month during the year CPP1, CPP2, and EI deductions stop for different salary levels ($75K, $100K, $150K). Title: 'When Does Your Paycheque Get a Boost in 2026?'"

Frequently Asked Questions

When do CPP deductions stop in 2026?

CPP1 deductions stop once your cumulative earnings in 2026 reach $73,200 (the Year's Maximum Pensionable Earnings, or YMPE). CPP2 continues for earnings between $73,200 and $81,900 (YAMPE). For most Canadians earning around $73,200–$90,000, CPP1 deductions stop between August and November depending on pay frequency.

What is the maximum CPP contribution for employees in 2026?

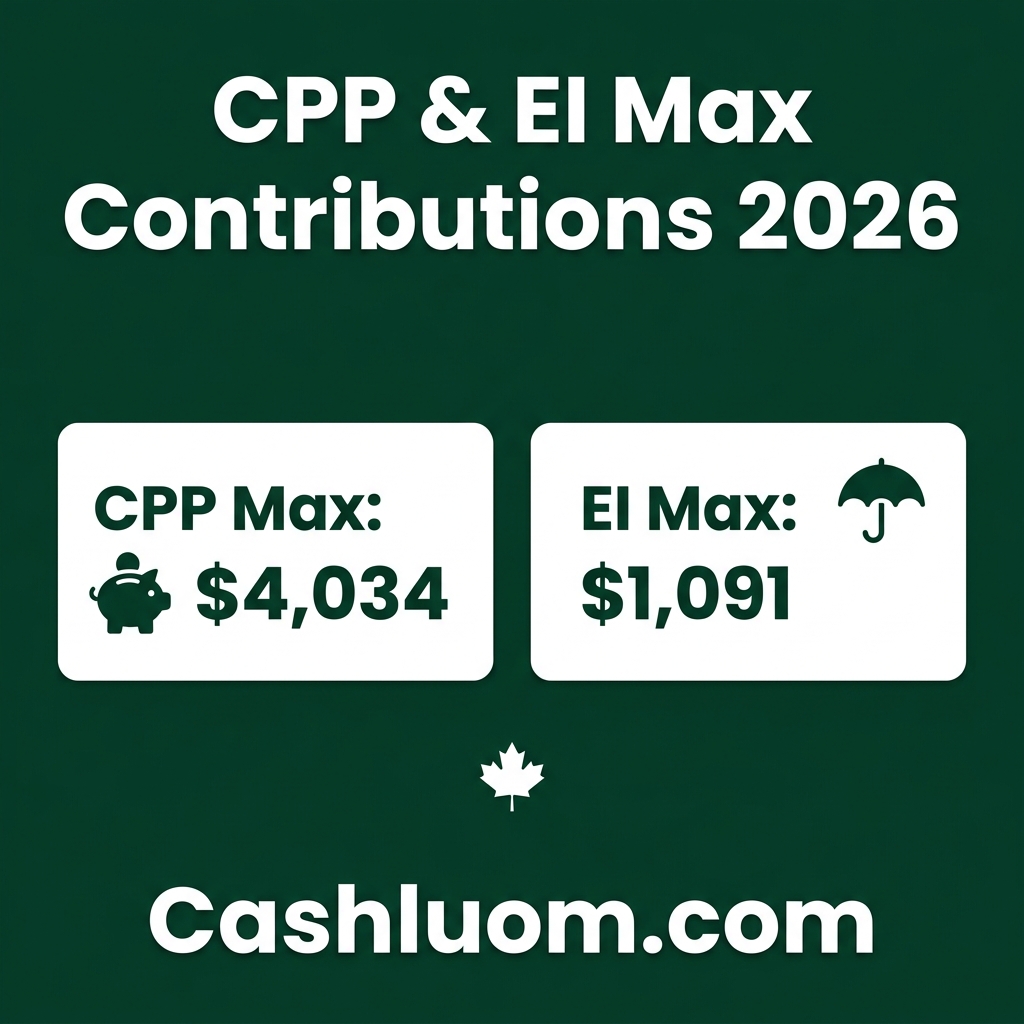

The maximum CPP1 employee contribution is $3,867.50 (5.95% on earnings from $3,500 to $73,200). CPP2 adds up to $347.00 (4% on earnings from $73,200 to $81,900). Total maximum CPP contribution for an employee in 2026 is $4,214.50. Your employer matches every dollar of CPP1 and CPP2 on top of that.

What is the maximum EI premium for 2026?

The maximum EI premium for employees in 2026 is $1,049.12 (1.66% on maximum insurable earnings of $63,200). Employers pay 1.4× the employee rate, so employer EI premiums cap at approximately $1,468.77 per employee. EI deductions stop once you've reached $63,200 in insurable earnings for the year.

Does my employer also stop paying CPP and EI when I hit the caps?

Yes. Your employer's CPP and EI contributions are linked to your earnings. Once you hit the thresholds, both you and your employer stop paying those contributions for the rest of the year. Payroll software tracks year-to-date earnings and automatically stops the deductions when the maximum is reached.

What is CPP2 and does it affect my 2026 paycheque?

CPP2 is the second tier of the enhanced Canada Pension Plan, contributing 4% on earnings between $73,200 and $81,900. It affects employees earning above $73,200: adding up to $347 more in total annual contributions compared to before 2024. However, CPP2 contributions also build a larger future CPP retirement benefit, specifically designed to provide higher income replacement for middle-to-upper earners.

I'm self-employed: how much CPP do I pay?

Self-employed Canadians pay both the employee and employer share of CPP. For CPP1: 11.9% (5.95% × 2) on earnings from $3,500 to $73,200 = max $7,735. For CPP2: 8% (4% × 2) on $73,200–$81,900 = max $694. Total maximum CPP for self-employed in 2026: approximately $8,429. Half of these contributions are deductible against business income; the other half generates a CPP credit.

Final Thoughts

The CPP and EI contribution caps are one of the clearest examples of Canada's progressive payroll system at work: you contribute a percentage of your earnings up to a ceiling, and once you hit that ceiling, you keep more of what you earn for the rest of the year. For higher earners, that mid-year pay boost can be $300–$700 per month. For self-employed Canadians, understanding the full double-rate structure is essential for quarterly tax planning. Use our Canada Salary Calculator to model your exact take-home, and read our full guide to CPP and EI rates for 2026 for a complete breakdown of every deduction line on your paycheque.

Sources & Citations

Free Calculator

Canada CPP & EI Calculator

Calculate your exact Canada Pension Plan (CPP) and Employment Insurance (EI) contributions for 2026.

Comments are coming soon. Have feedback? Contact us.