For many Canadian workers, the start of a new year brings a subtle disappointment: a smaller-than-expected first paycheck. This "January shrinkage" is almost always caused by the reset of Canada Pension Plan (CPP) and Employment Insurance (EI) deductions. In 2026, the impact is more pronounced as we enter the second full year of the "CPP2" additional contribution tier. While these deductions are often viewed as a burden, they are the bedrock of Canada's social safety net. This guide breaks down the technical mechanics of 2026 payroll deductions and reveals how much you will really pay over the course of the year.

Total Payroll Burden = (Earnings × 5.95% CPP) + (Earnings × 1.66% EI) + CPP2

Employers must match your CPP contributions dollar-for-dollar and pay 1.4x your EI premiums.

The CPP Enhancement: Understanding Tier 1 vs Tier 2

The most significant change to Canadian payroll in recent decades is the "CPP Enhancement," which began in 2019 and reached its final phase in 2024. For the 2026 tax year, every employee is contributing more than they did five years ago, but they are also earning significantly higher pension entitlements for the future.

- Tier 1 (Base CPP): You pay 5.95% on your earnings between $3,500 and the Year's Maximum Pensionable Earnings (YMPE). For 2026, the YMPE is expected to be approximately $71,000.

- Tier 2 (CPP2): If you earn more than the YMPE, you pay an additional 4% on the slice of income between the YMPE and a second, higher ceiling known as the Year's Additional Maximum Pensionable Earnings (YAMPE). For 2026, the YAMPE is roughly 14% higher than the first ceiling (approx. $81,000).

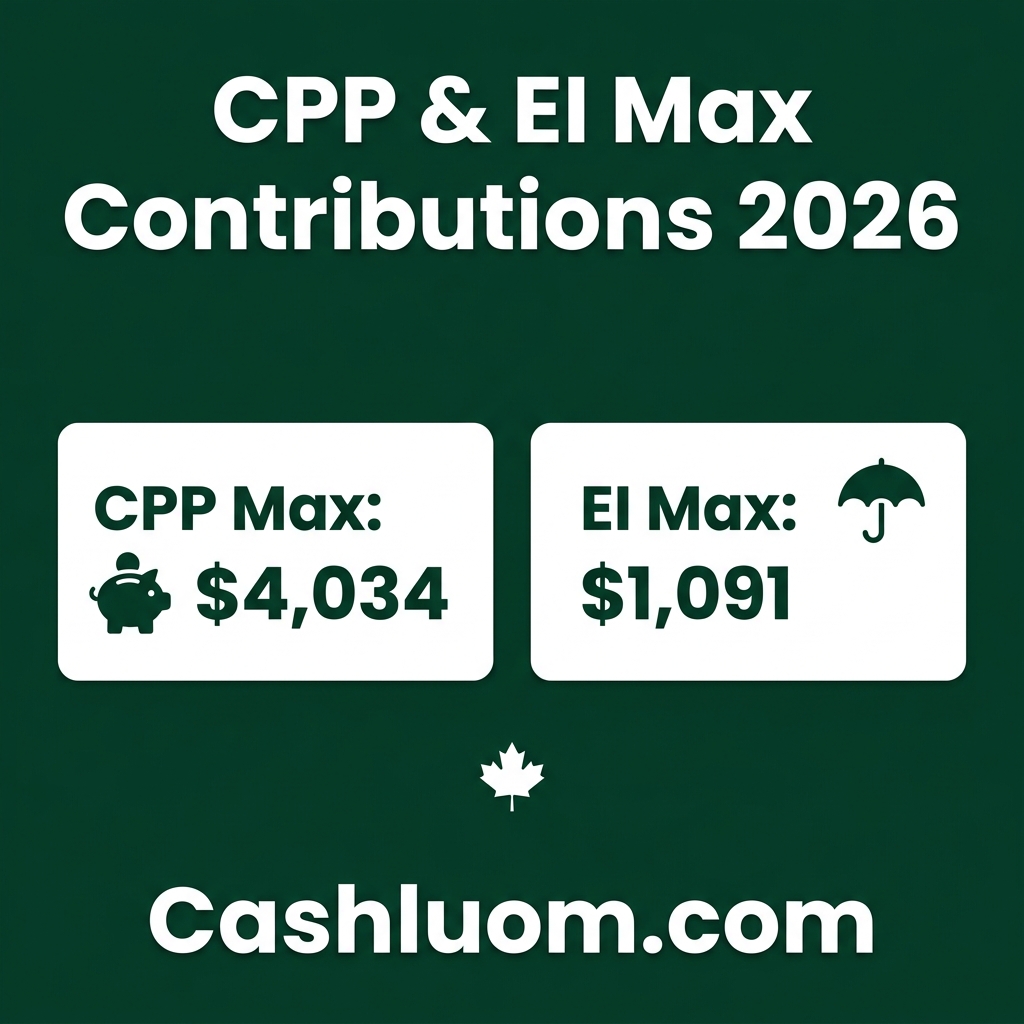

The goal of this "double-tier" system is to replace 33% of your average pre-retirement earnings, up from the original 25% target. For high earners, this means an annual CPP bill that can exceed $4,000 for the employee portion alone.

Employment Insurance (EI) in 2026: Rates and Benefits

Employment Insurance is your mandatory insurance policy against job loss, sickness, and parental leave. For 2026, the premium rate for employees is approximately 1.66% (excluding Quebec, which has its own rate). The premiums are capped once you reach the Maximum Insurable Earnings (MIE) threshold, which for 2026 is projected to be around $65,500.

The "max premium" for 2026 is expected to be roughly $1,085 per year. The trade-off for these premiums is the weekly benefit amount. If you qualify for EI in 2026, your weekly benefit is 55% of your average insurable weekly earnings, up to a maximum payout of approximately $685 per week. This provides a critical buffer during career transitions.

| Deduction Type | 2026 Rate | Annual Max (Est.) | Employer Match |

|---|---|---|---|

| Base CPP | 5.95% | $4,020 | 100% ($4,020) |

| CPP2 (Additional) | 4.00% | $400 | 100% ($400) |

| EI Premium | 1.66% | $1,085 | 140% ($1,519) |

| Combined Total | - | $5,505 | - |

The "Paycheck Bump" Phenomenon

One of the most satisfying moments for Canadian workers earning over $85,000 is the "Paycheck Bump." Because CPP and EI contributions have annual maximums, high earners will eventually "max out" their contributions partway through the year.

For example, an executive earning $150,000 will likely hit their EI cap in June and their CPP caps in August. Starting in September, the 5.95% and 1.66% deductions disappear from their paystub. This results in a sudden, significant increase in net take-home pay for the final months of the year—effectively a "tax holiday" until the counter resets on January 1st of the following year.

Frequently Asked Questions

Can I opt-out of CPP or EI in 2026?

Generally, no. If you are an employee between the ages of 18 and 65 (or up to 70 if you haven't started receiving CPP), these deductions are mandatory by federal law. The only major exception is for certain members of religious orders or self-employed individuals who choose not to opt-into the EI program.

What happens if I overpay my CPP or EI?

If you have multiple jobs or changed employers mid-year, you will likely overpay your premiums. Don't worry—any overpayment is automatically calculated when you file your income tax return (T1) and is returned to you as a tax refund.

Is the CPP2 deduction tax-deductible?

Yes. Contributions to the "enhanced" portion of CPP (including CPP2) are fully tax-deductible, meaning they reduce your taxable income. Contributions to the "base" portion of CPP earn you a non-refundable tax credit at the 15% rate.

Do seniors still pay CPP after they start receiving benefits?

If you are between 60 and 65 and still working while receiving CPP, you must still contribute. If you are between 65 and 70, you can choose to stop contributing by filing a specific CPT30 form with your employer.

Why is the EI rate different in Quebec?

Quebec operates its own parental insurance plan (QPIP). Because the federal EI program doesn't have to pay for parental benefits in Quebec, the EI premium rate for Quebec residents is reduced (approx. 1.32% in 2026).

Managing your expectations around payroll deductions is the first step to successful financial planning. While the numbers on your paystub may change throughout the year, knowing exactly when and why those changes occur allows you to budget with precision.

Want to see your exact 2026 deduction schedule? Use our Canada Salary Calculator to find out exactly which month you'll hit your CPP and EI caps based on your current salary.

Sources & Citations: Content verified against official guidelines from the IRS (US), HMRC (UK), and ATO (AU). Information is reviewed for accuracy prior to publication.

Free Calculator

Salary Calculator

Calculate your exact net take-home pay after all government deductions. Our salary tool handles UK PAYE/NI, US Federal/State taxes, Australian ATO rates, and more. Enter your gross annual pay to see your monthly, bi-weekly, and weekly cash in hand. Updated for the latest 2026 tax brackets and social security thresholds.

Comments are coming soon. Have feedback? Contact us.