W2 vs 1099 Take-Home Calculator — 2026

Estimates only. Consult a tax professional for your specific situation. Federal brackets are 2026 single-filer rates with $15,000 standard deduction.

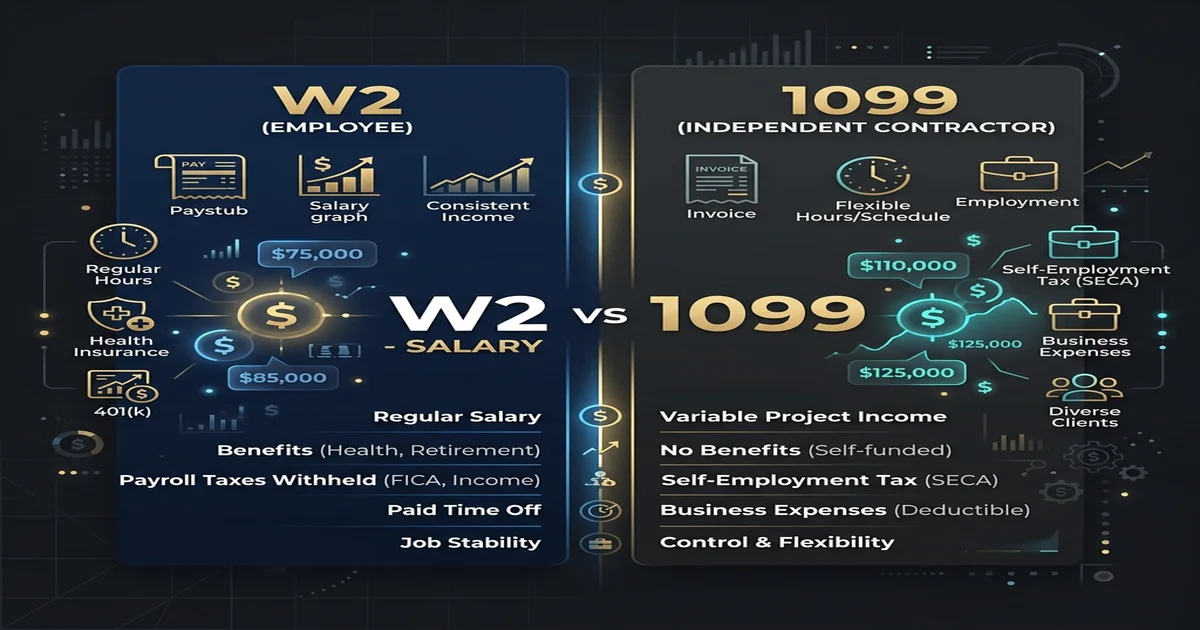

The decision between W-2 employment and 1099 contracting is one of the most financially significant choices an American worker can make. A $100,000 W-2 salary and a $100,000 1099 contract are not equivalent: the 1099 contractor pays self-employment tax on top of income tax, must fund their own retirement plan, buy their own health insurance, and manage quarterly tax payments. But 1099 work also comes with deductions unavailable to employees. This guide compares both structures with actual numbers so you can make an informed decision.

Self-Employment Tax Rate

SE Tax = 15.3% on 92.35% of net self-employment income (up to SS wage base)

12.4% Social Security + 2.9% Medicare on 92.35% of net self-employment income. You can deduct 50% of SE tax paid as a business expense on Schedule 1, reducing your taxable income.

W-2 vs 1099: Side-by-Side Comparison

| Feature | W-2 Employee | 1099 Contractor |

|---|---|---|

| Gross payment received | $100,000 | $100,000 |

| Social Security (6.2%) | −$6,200 (withheld) | −$12,400 (both shares) |

| Medicare (1.45%) | −$1,450 (withheld) | −$2,900 (both shares) |

| Federal income tax (est. 22%) | ~−$14,683 | ~−$13,000 (after SE deductions) |

| Health insurance | Often employer-subsidized | Full premium ($600–$1,000+/month) |

| Retirement (401k) | Employer match available | Solo 401k or SEP-IRA, self-funded |

| Business expense deductions | Very limited | Extensive — home office, vehicle, equipment, etc. |

| Estimated taxes required | No — withheld automatically | Yes — quarterly IRS payments |

| Net take-home (approx.) | ~$78,000 (before benefits) | ~$65,000–$73,000 (before health insurance) |

⚠️ Single filer in a moderate-tax state (e.g., Texas or Florida, no state income tax). Federal income tax estimate based on 2026 brackets. Actual results vary significantly by state, deductions, and benefits. Source: IRS. Self-Employment Tax.

How Much More Does a 1099 Contract Need to Pay?

To achieve equivalent net take-home to a W-2 salary, a 1099 contractor needs a significantly higher contract rate. The exact premium depends on your income level, health insurance costs, retirement contributions, and state taxes, but as a rule of thumb:

| W-2 Salary Equivalent | Required 1099 Rate (No Benefits) | Required 1099 Rate (With Benefits Costs) |

|---|---|---|

| $60,000 | ~$74,000–$78,000 | ~$86,000–$96,000 |

| $80,000 | ~$98,000–$103,000 | ~$113,000–$130,000 |

| $100,000 | ~$122,000–$128,000 | ~$140,000–$160,000 |

| $150,000 | ~$177,000–$188,000 | ~$195,000–$220,000 |

⚠️ Estimates vary by state tax, health insurance premium, retirement contribution amounts, and actual business expenses. The "with benefits" column includes approximate employer-equivalent health insurance and retirement match. Ranges reflect different tax situations. Use these as starting points for negotiation, not precise equivalents.

Key 1099 Contractor Tax Advantages

Despite the higher self-employment tax burden, 1099 contractors have access to deductions that W-2 employees cannot claim:

- Home office deduction: If you have a dedicated workspace used exclusively for business, you can deduct a proportionate share of rent/mortgage, utilities, and internet: no T2200 equivalent required (Schedule C and Form 8829)

- Vehicle expenses: Business use of a personal vehicle via mileage rate (67 cents/mile in 2024; check 2026 rate) or actual expense method

- 50% of SE tax deduction: Half of self-employment tax is deductible from gross income on Schedule 1: partially offsetting the extra SE tax burden

- Health insurance premiums: Self-employed people can deduct 100% of health insurance premiums for themselves and family as an adjustment to income

- SEP-IRA / Solo 401k: 1099 workers can contribute up to $69,000/year (2024 limit) to a Solo 401k: far exceeding W-2 employee 401k limits of $23,000: with the entire contribution being tax-deductible

- QBI Deduction (Section 199A): Eligible self-employed workers can deduct up to 20% of qualified business income from taxable income: a powerful deduction that W-2 employees cannot access

Frequently Asked Questions

What is self-employment tax in the US in 2026?

Self-employment tax is 15.3% of 92.35% of your net self-employment income: up to the Social Security wage base (~$176,100 in 2026). It consists of 12.4% Social Security + 2.9% Medicare. Above the SS wage base, only the 2.9% Medicare portion applies (plus 0.9% Additional Medicare Tax if income exceeds $200K single/$250K MFJ). You can deduct 50% of the total SE tax paid as an adjustment to income on Schedule 1.

Do 1099 contractors get a tax refund?

1099 contractors can get a refund if their quarterly estimated tax payments (or any withholding on backup withholding) exceeded their actual annual tax liability. However, most self-employed people carefully calibrate their quarterly payments to minimize over- or under-payment. A large refund as a 1099 contractor generally means you were giving the IRS an interest-free loan throughout the year: it's better to pay accurately quarterly and keep the money working for you.

Can a 1099 contractor contribute to a 401k?

Yes: through a Solo 401k (also called Individual 401k) or a SEP-IRA. A Solo 401k lets you contribute as both "employee" (up to $23,000 in 2024, $30,500 if over 50) and "employer" (up to 25% of net self-employment income), with a combined annual max of $69,000 ($76,500 if 50+). This far exceeds what W-2 employees can contribute to a standard 401k, making the Solo 401k one of the most powerful tax-sheltered vehicles for high-earning contractors.

What's the break-even hourly rate for a 1099 contractor vs W-2 employee?

A simple rule of thumb: multiply your equivalent W-2 hourly rate by 1.25–1.35 for a raw break-even on taxes and FICA, then add your estimated health insurance and retirement costs on top. For a $50/hour W-2 worker with good benefits: a 1099 equivalent might need to be $75–$90/hour to truly match the net compensation and benefits value. Use the comparison tables above to model your specific income level.

Can you switch from W-2 to 1099 for the same employer?

Only if the working arrangement genuinely changes: the IRS has strict worker classification rules (the "ABC test" and common law factor test). Converting an employee to a contractor purely to reduce payroll taxes without changing the work relationship is illegal (worker misclassification). The IRS looks at behavioral control, financial control, and type of relationship. Misclassified workers can file Form SS-8 to have the IRS determine their status, and employers face back taxes, penalties, and interest for misclassification.

Final Thoughts

The W-2 vs 1099 decision is ultimately a personal financial engineering question: do the higher self-employment taxes and benefit costs of contracting get offset by higher pay rates and better deductions? For most skilled professionals in high-demand fields (tech, consulting, healthcare), 1099 contracting at the right rate generates more net wealth, but only if you're disciplined about quarterly taxes, retirement savings, and health insurance costs. Use our US Income Tax Calculator to model your specific scenario, and read our self-employed tax guide (for Canadian contractors) or consult a US CPA for personalized advice.

- Salary Calculator. Convert annual salary to monthly, weekly, and hourly take-home pay after taxes

- Salary to Hourly Calculator. Find your true hourly equivalent and set your 1099 rate with confidence

- Inflation Calculator. See how your contractor rate holds up against inflation over time

Sources & Citations: Content verified against official guidelines from the IRS (US), HMRC (UK), and ATO (AU). Information is reviewed for accuracy prior to publication.

Free Calculator

Salary to Hourly Calculator

Convert any annual salary to a precise hourly rate. Ideal for freelancers, contractors, and employees negotiating new contracts. Enter your annual pay and work hours to see exactly what you earn per hour, day, and week. This tool accounts for standard work weeks and helps you compare salary offers more effectively.

Comments are coming soon. Have feedback? Contact us.